function G=pass(X) % G=1 means pass, G=0 fail, X vector with hand-in scores

M=[M1, M2, M3, M4, M5, M6]; % maximum on each hand-in

S=sum(X); % total points

G=1;

for i=1:6

if X(i)<0.3*M(i)

G=0;

end

end

if S< 0.5*sum(M)

G=0;

end

| No 1. | September 7 ps-file, pdf-file. Solutions ps-file, pdf-file. |

| No 2. | September 14 ps-file, pdf-file. |

| No 3. | September 21 ps-file, pdf-file. Solutions ps-file, pdf-file. |

| No 4. | September 28 ps-file, pdf-file. Solutions ps-file, pdf-file. |

| No 5. | October 5. Exercises 4.1,7,9,18 and 5.1,3 in Klebaner. |

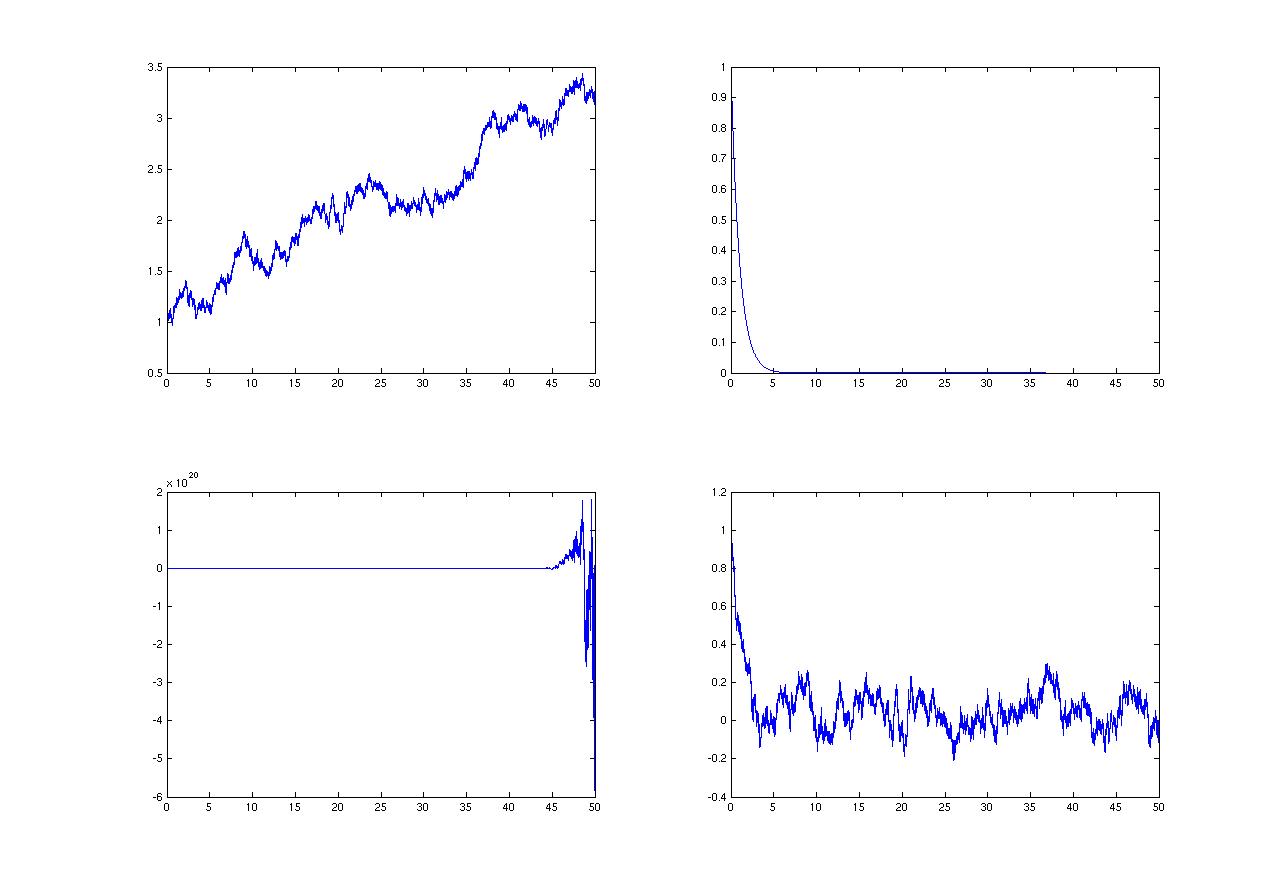

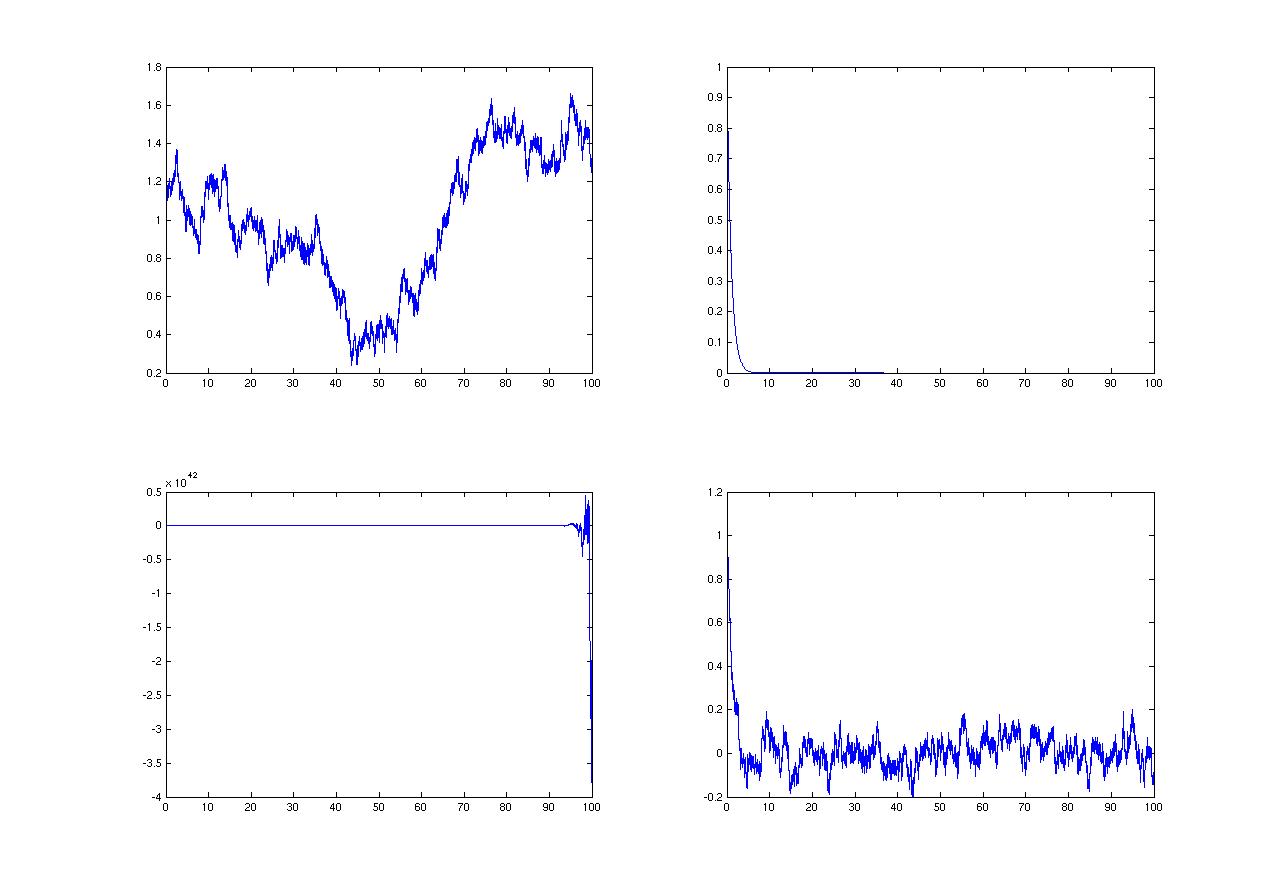

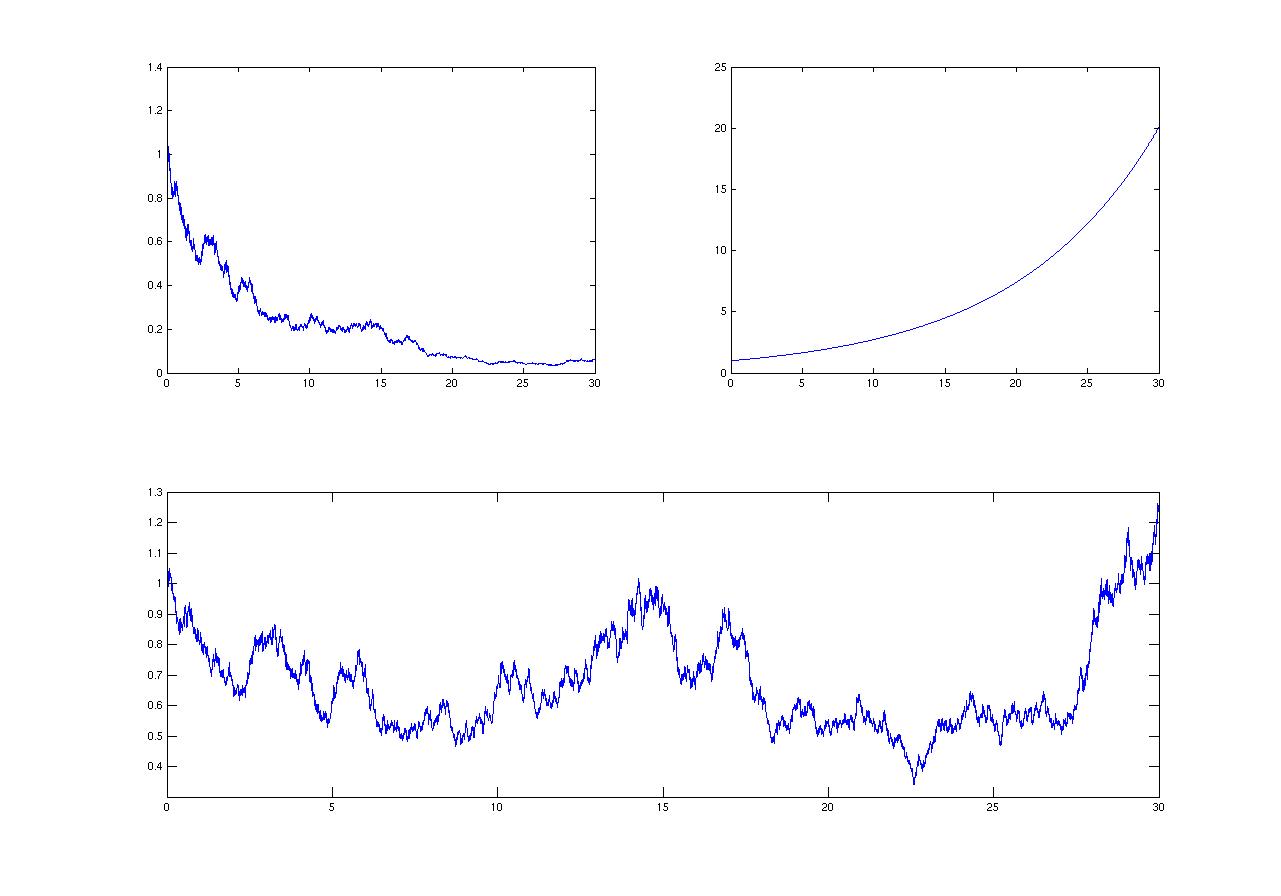

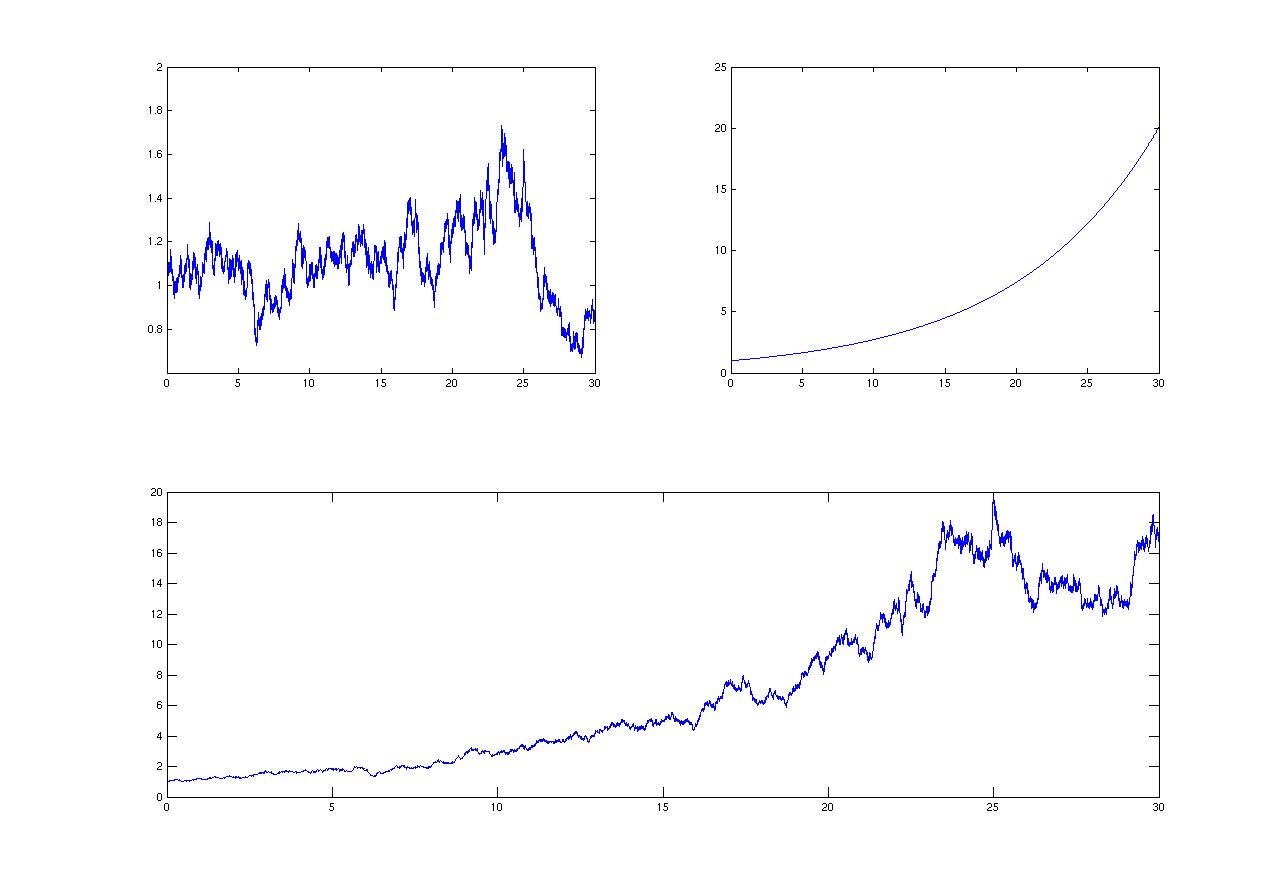

| No 6. | October 10, Wednesday! ps-file, pdf-file. We look at examples of an SDE with stationary distribution (Ornstein-Uhlenbeck) and one without (Black-Scholes). The Matlab simulations can be found here: Ornstein-Uhlenbeck, pictures 1, 2, 3. Black-Scholes, pictures 1, 2. |

Course Programme ps-file,

pdf-file,

dvi-file.

Daniel Ahlberg is responsible for exercises and hand-ins. If you have any doubts or questions, you are welcome to contact me.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}